As lockdown restrictions roll into September, we’re finding ourselves turning to the bookshelf/kindle for some distraction, inspiration, and personal growth. After all, binge watching and gardening can only take up so many hours a day. There are a vast number of personal finance books out there to help you be better, wiser, and wealthier with your money.

Many can be quite self-serving or questionable (if you really “have the secret formula and are so wealthy”, why are you sharing again?) but there are a few classics out there that can provide great insights into how you can manage your money and invest smarter.

Without further ado, here is the Kernel team’s favourite personal finance books, all available for download to Kindle or audiobook.

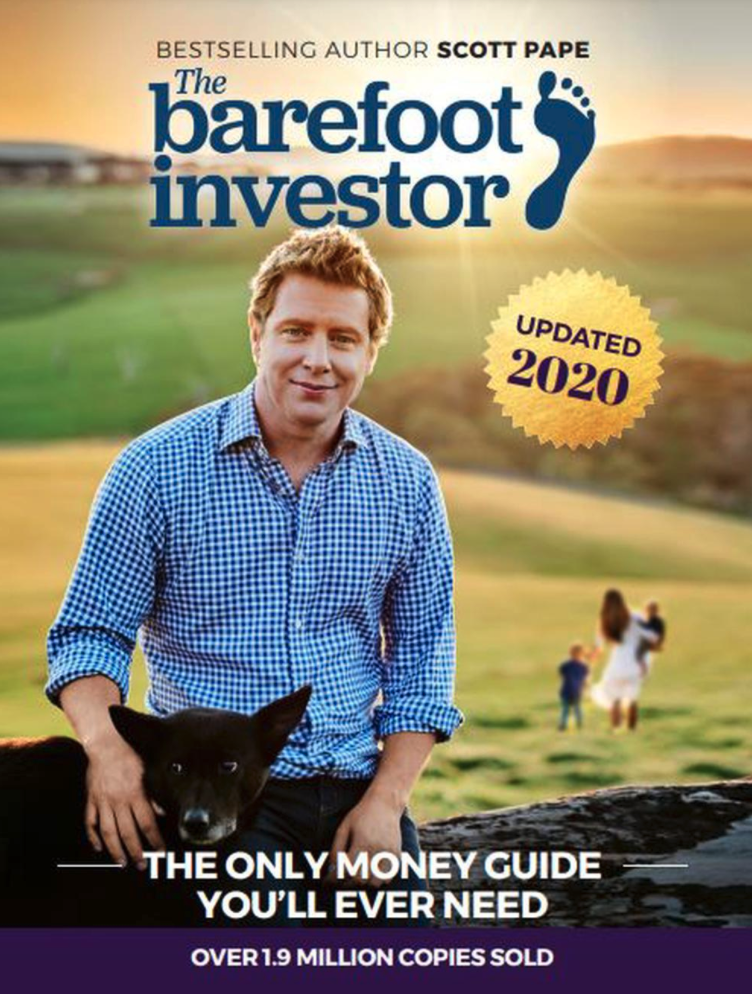

The Barefoot Investor – Scott Pape

This book, written by Australian celebrity financial planner is humorous and an excellent starting place for anyone wanting to learn the basics of good individual money habits, especially for those in their 20’s and 30’s.

The blueprint is simple, live a basic life off 60% of your after-tax income, keep 20% for the unexpected, invest 10% for the long term and enjoy 10% for splurges. While we disagree with the promotion as the only money guide you’ll ever need, joining the barefoot tribe will help you with the habits and discipline to get going in the right direction.

Our biggest takeaways? Firstly, one of the most dangerous things you can do (especially men) is expect or want to go from 40 hours a week work to zero hours a week in retirement. Instead, it’s better to have options to do the work you want. The second takeaway is that it’s all about achievable habits and routines, as willpower is like a muscle that becomes fatigued from overuse.

Check out the Barefoot Investor here.

Rich Enough? – Mary Holm

Mary Holm is a well-known New Zealand personal finance journalist and host of the “Your Money with Mary Holm” podcast. We believe this straightforward Kiwi-orientated guide should be on everyone’s reading list and part of our secondary school curriculum.

It covers all the key topics of debt, emergency savings, investing (spoiler: she’s a big fan of index investing), KiwiSaver and buying or not buying a house. The key insight, beyond a certain point, is that having more money is not the key to happiness, and sometimes the opposite.

Mary has also recently published a sequel, “A Richer You”, which is a great next step to continue on your reading journey.

Check out Rich Enough? here.

The Millionaire Next Door: The Surprising Secrets of America’s Wealthy – Thomas Stanley

Based on fascinating research about who was truly wealthy and who was all show and no dough i.e. all debt fuelled. This New York Times bestseller is a great counterpoint to “keeping up with the Jones” or social climbing.

It points out that since the twentieth century and even more so in the age of social media, there is much illusion of wealth and that many outwardly “rich” Americans are actually drowning in debt for their possessions.

Our favourite saying from the book is don’t be “Big Hat, No Cattle” especially if you want mental and physical wellbeing. It also doesn’t mean only being frugal, it means financial freedom from having a “Go to hell” fund.

Check out The Millionaire Next Door here.

Thinking Fast and Slow – Daniel Kahneman

This huge bestseller by the first psychologist to win the Nobel Prize in Economics, is a tour of the mind and how our irrationalities and emotive decisions are actually rational.

Ground-breaking for the field of Behavioural Economics, the concepts of loss aversion, herding and availability heuristics are all truly relevant to investing. Most well-known for the concepts of System 1 and 2, where most decisions are System 1 fast, intuitive, emotional and biased; whereas System 2 is slower, more deliberative, more logical, and recognising our human failings and that of others.

Check out Thinking Fast and Slow here.

The Little Book of Common Sense Investing – John Bogle

Written by the founder of Vanguard, John Bogle, this is a best-selling guide to getting smart about the market. While written from an American perspective, where New Zealand’s tax environment and market dynamics mean that different strategies are more appropriate, there are number of tips and explanations that are brilliant.

Warren Buffett said this about Bogle: “If a statue is ever erected to honour the person who has done the most for American investors, the hands-down choice should be Jack Bogle. For decades, Jack has urged investors to invest in ultra-low-cost index funds. Today, however, he has the satisfaction of knowing that he helped millions of investors realize far better returns on their savings than they otherwise would have earned. He is a hero to them and to me.”

Check out The Little Book of Common Sense Investing here.

The Power of Passive Investing – More Wealth with less work – Robert Ferri

A well-researched investigation of why picking individual shares is futile for the vast majority of investors and why, at scale, fund managers can’t beat the market.

This thorough book with chapters for individuals, trusts, and advisers comprehensively explains the futility of spending time seeking alpha, and why profits and incentives lead to misleading advertising. Ferri also explains where value can truly be added, thorough good asset allocation, education and productive, not destructive behaviours. The bottom line is your bottom line.

Check out The Power of Passive Investing here.

Where Are The Customers’ Yachts? – Fred Schwed Jr.

This timeless classic from 1940 remains a fascinating read and an illustration of how little has changed in the financial markets – greed, fear, and stupidity still rule the roost of individual investors.

Fred’s own experience of Wall Street feeds into the folklore of this book, with his cynicism about the entire financial profession clearly on display in the title carrying throughout the book.

This critical view of the financial profession also holds some truths for the everyday investor, highlighting that the biggest problem for most investors is controlling their own emotions. The ability to sit still is a superpower, with most people suffering from an inability to do nothing. Re-enforcing that the best portfolio is the one you will actually stick with – set and forget. A challenge in a digital world of anywhere, anytime access.

Check out Where Are The Customers’ Yachts? here.

The Simple Path to Wealth – JL Collins

This book is a consolidated version of his blog, with one of his most popular reads “Why you need f-you money” becoming viral after its inclusion in the movie “The Gambler” (language warning).

A combination of personal finance principles combined with a simple investment guide; the book is designed to set readers on a path to financial independence. While written for the American reader, with its emphasis on a US total stock market fund as the core building block, the key investment philosophy holds true for all readers: No one can reliably time the market. No one can reliably pick individual stocks over time. No one can reliably pick the next winning active fund manager. Therefore, adopt a simple, proven, and effective strategy for accruing wealth through the core use of index funds.

Check out The Simple Path to Wealth here.

The Richest Man in Babylon – George Clason

George Samuel Clason is an author from the early 1900’s who revolutionized financial advice when he started writing pamphlets about achieving financial success.

The Richest Man in Babylon is a compilation of this work, written as a collection of parables set in ancient Babylon. Centred on the fictional character Arkad, a poor scribe who became the ‘richest man in Babylon’, George details the secret to creating wealth is spending as little as possible, saving money so you can invest, and investing in yourself so you can seize opportunities as they arise, concepts that hold true nearly 100 years after the book was first released.

George is also credited with inventing the term ‘Pay yourself first’, a concept we are strong proponents of and have written on in several of our blogs.

Check out The Richest Man in Babylon here.

And for the advanced – Capital in the 21st Century – Thomas Piketty

An absolute tome. Hard going at times but brilliant economic analysis overall. Without attempting to distil into a few sentences, this book explains inequality and its increase based on 300 years of data worldwide. But also, why ownership (of property, shares and/or share funds) is key to personal wealth. However, economic trends are not acts of God or unchangeable, political action has curbed dangerous inequalities in the past.

Check out Capital in the 21st Century here.

Bonus: For those who enjoy history and want to develop a deeper understanding of the financial markets we highly recommend Bulls, Bears and Elephants: A History of the New Zealand Stock Exchange. A great summary of the history of New Zealand’s capital markets, from the early gold mining boom and dozens of stock exchanges scattered throughout NZ, through to the excesses and lack of regulatory scrutiny of the 1980s. This book will give you a greater appreciation of our wild west roots and why so many New Zealanders had a negative view of investing in shares and felt the stock market was for gamblers. This book is hard to get hold of, but occasionally can be found at second-hand stores or currently through Victoria University here.

But how does this apply in NZ?

Our recommended personal finance books contain several shared principles that all investors can follow to help build their long-term wealth, regardless of whether you’re based in the country of which they were written. These can be summarised as:

1. Pay Yourself First: At its simplest pay yourself first means: Every payday, the very first thing you do is set aside a regular amount of money for future you. Before you pay any bills, rent or mortgage, go out for dinner or head to happy hour. As per the Barefoot Investor, live a basic life off 60% of your after-tax income, keep 20% for the unexpected, invest 10% for the long term and enjoy 10% for splurges.

2. Control Your Expenses: To save and invest a minimum of 30% of your earnings, you will have to control the money going out. This means learning to live below your means and try to avoid unnecessary expenses. This does not mean you need to stop the daily takeaway coffees or weekend avocado on toast, instead, it is about balance. Focus on the larger expense items, regularly invest where you can, and remember you do not need to start out saving 30%, you can build to this over time at a pace you are comfortable with.

3. Make Money Work for You: The reality is not spending unnecessarily and saving money into the bank is not enough to secure your financial future. But it does provide you will the money you need to invest for future you. Every spare cent, above an emergency savings account, should be directed towards your investment goals. If you do this, and if you make sound investment decisions, your saved money will increase considerably.

A proven way to build long term wealth is through index funds, recommended by a number of personal finance books above. While most of the books are US centric, with a focus on US based funds due to the tax efficiency for domestic investors, you can apply the same principles to an NZ strategy.

If you were looking to replicate the Barefoot Investor or A Simple Path to Wealth strategy, you would start with a well-diversified NZ index fund, such as Kernel’s NZ 20 Fund or NZ 50 ESG Tilted Fund, and then support this with a broadly diversified global fund such as our S&P Global 100 or S&P Global Dividend Aristocrats funds. These funds can form the core foundation of an investment portfolio which you can then add to over time to suit your own circumstances.

4. Protect Your Wealth: Investing involves risk, in fact, some risks are reasonable, as the higher the risk, the higher the rewards. However, that does not mean you need to be concerned about losing your entire investment. What you need to do is minimise the controllable risks. One way to do this is to diversify, which means spreading your investment across a number of companies, sectors, and countries through a handful of well diversified index funds. This will ensure your future wealth is not reliant on the success of one single investment decision or one single company.

The common theme of the personal finance books above is the emphasis on simple and proven investment strategies that you regularly contribute to and do not touch. Simple in theory, hard in practice.

Take your time to set out a logical plan that you can work towards and then stick to it. Focus on the four points above. Do not over complicate it, avoid constantly looking at your investment portfolio, and focus on the things you can control. In the end, the purpose of this work is to enjoy a prosperous financial future, that doesn’t need to come at the sacrifice of enjoying your life now.